Confronted by the economic slowdown and rising prices, foodservice distributors find themselves caught in the middle of the food system value chain—pressured by both suppliers and buyers.

Manufacturers increasingly are passing on higher commodity and product prices, while restaurant operators, responding to consumer demands, are adjusting their buying habits in favor of lower-priced food items. At the same time, foodservice distributors face increased competition from new and stronger distribution organizations.

In October, 2008, Chicago-based West Monroe Partners conducted an analysis of the foodservice distribution industry using publicly available research and information. The results spotlight the key trends affecting foodservice distributors’ operations today and the opportunities they have to cut costs, improve productivity, and increase competitiveness. In particular, foodservice distributors have a significant opportunity to counteract market pressures and improve operations by focusing on one of their largest expenditures—labor.

FOODSERVICE DISTRIBUTION INDUSTRY TODAY

Three primary types of organizations comprise the $225 billion foodservice distribution industry:

• Broadline foodservice distributors—companies that traditionally have purchased a wide range of food products from manufacturers. Most broadline distributors offer value-added services designed to meet the needs of single-store restaurants and small chains.

• Specialty distributors—companies that do not stock a wide range of products; instead, they operate in niche markets in which it is necessary to have specialized knowledge about the product(s) handled or the operator(s) served.

• System distributors—companies that serve a customer base consisting primarily of chain restaurants with centralized purchasing and menu development functions; thus, these customers typically don’t require specialized services.

The industry is relatively concentrated, with the top 20 organizations accounting for 34 percent of revenues in 2007.

Total foodservice distribution revenues declined in 2007, down three percent from the year before. Broadline distributors, however, have grown faster than the market, as depicted below. Supported by innovations and effective marketing efforts, leading broadline foodservice wholesalers/distributors—the 36 largest companies in this category—registered a consistently higher growth rate compared to the food services industry as a whole during the period from 2002 to 2006.

CHANGING ENVIRONMENT SQUEEZES MARGINS

West Monroe Partners’ analysis confirmed that a variety of trends—from shifting consumer tastes and value demands, to rising food prices, to increased competition from new and larger competitors—are forcing foodservice distributors to adapt their operations.

At the same time, the weakening economy has eroded consumer confidence, a factor that may interrupt what has been a positive trend for foodservice distributors—steady, long-term growth in consumer spending on food away from home. According to a Booz & Co. survey, more than one third of consumers have made substantial cutbacks in frequent purchases during 2008.

Altogether, these trends have had a marked effect on foodservice distributors’ margins. Some major industry players have witnessed double-digit declines in gross profit margin over the past several years.

Evolving consumer spending habits and tastes are driving new product and competitive strategies.

Food expenditures in the United States have increased steadily since 1990 along with growth in the country’s population; however, per capita food expenditures have grown at a much slower rate. While food spending is up, consumers are spending less of their disposable income on food. Food expenditure as a share of disposable personal income declined from 12.6 percent in 1990 to 11.4 percent in 2007.

Over the same period, consumers have shown a growing preference for eating out, effectively closing the gap between spending on food consumed in the home versus food consumed away from home.

Finally, consumers increasingly are demanding value, convenience, and organic and eco-friendly products. For example, sales of organic food and beverages grew from $1 billion in 1990 to an estimated $20 billion in 2007. Private-label goods also are gaining share—accounting for about 16 percent of all U.S. food sales in 2007. These shifts are forcing foodservice distributors to refocus their product and branding strategies and confront new competitors, such as supermarkets and convenience stores.

Customers are counteracting rising food prices by demanding lower-priced food items for their menus.

According to U.S. Bureau of Labor statistics, wholesale food prices rose 8.2 percent during the first six months of 2008, up from 7.6 percent for all of 2007—a result of rising oil prices, demand from rapidly developing economies, and a larger share of the grain market going to ethanol production. As a result, foodservice companies and their customers are developing concepts that utilize lower priced items, such as less expensive cuts of meat and seasonal produce.

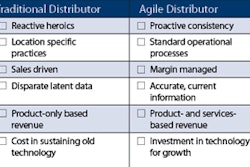

Distributors are improving technology and operations.

Today’s customers demand lower prices, but without altering their service expectations. To compensate, food distributors increasingly are investing in systems and technology and improving their supply chains.

Industry consolidation is producing fewer, but many more formidable, competitors.

The industry’s needs to scale operations, cater to larger customers, and serve wider geographic territories have produced a moderate and steady level of acquisition activity. Continuing consolidation of grocery stores and the growth of national chain restaurants also have encouraged consolidation among foodservice distributors. Private equity deals in the U.S. food industry reached a peak in 2007.

Eliminate indirect activities.

Foodservice distributors lose a large amount of productive time to indirect activities—usually the product of inefficient processes—performed by order selectors and forklift operators over the course of their work day. These activities raise the cost of operations. With proper training, frontline managers can identify and remedy these situations.

Apply discrete engineered labor standards.

Discrete engineered labor standards define, scientifically, the time required to accomplish a given task—information that can improve the way a company manages workforce productivity, plans and schedules work, and compensates workers. Traditional standards, which are based on Key-Value-Indicators (KVIs), aren’t enough. Discrete standards remove averages all together and provide the highest level of value in managing labor costs—sometimes as much as 15 to 20 percent over KVI-based systems.

Train managers to manage the workforce.

Managers at all levels must be able to direct the workforce properly, and supervisors must be able to recognize and address day-to-day impediments and schedule workers in a way that lowers overtime and increases service levels. Proper management training can improve these processes.

Train employees to apply proper methods.

Establishing a high performance environment requires training employees to work in an optimal fashion—for example, teaching order selectors how to improve their methods so that they can work at a faster pace.

Rationalize SKUs.

Distributors face a constant battle between merchandisers and operators over the optimal number of SKUs; for example, how many different types of canned tomatoes must a distributor carry in order to satisfy clients’ needs? Delisting SKUs can lower inventory costs and shorten pick paths to improve productivity. Rationalization starts with an unbiased, systematic analysis of SKUs, looking for opportunities to lower costs and improve efficiency.

Implement activity-based compensation.

Activity-based compensation—pay or incentives for performance—increases productivity, accuracy, and assiduity. A well-established program benefits employees and the company, but it is important to have the proper baselines in place beforehand to ensure that the program is attractive to employees and lucrative for the company. Solid discrete standards are paramount to this approach.

NAVIGATE THE THREATS

West Monroe Partners’ comprehensive 2008 analysis of the food distribution industry reveals a landscape of both opportunities and threats. While consumer spending on food away from home continues to follow a long-term upward trend, a variety of factors—from changing tastes, to rising food prices, to industry consolidation—are putting extreme pressure on distributors’ profit margins. Analyzing and optimizing labor costs can help foodservice distributors counteract market forces by reducing costs and establishing flexible, competitive operations.

Food service distributors can counteract shrinking margins by optimizing labor costs.

The combination of shrinking margins and a weak economy mandates swift changes to the distribution environment and practices in order to reduce costs.

While technology initiatives can produce significant efficiency improvements and, ultimately, lower costs, these efforts typically require a sizeable investment and a long lead time. Labor costs, on the other hand, represent at least half of a distributor’s total spending. Applying certain labor management strategies, such as those described below, can help foodservice distributors achieve significant short-term cost savings and improve their margins.